Description

In this market risk course online, we delve into the principles of liquidity risk measurement and management, and explore the impact on bank performance of the framework set by Basel.

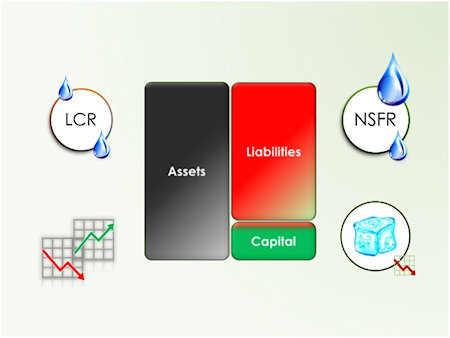

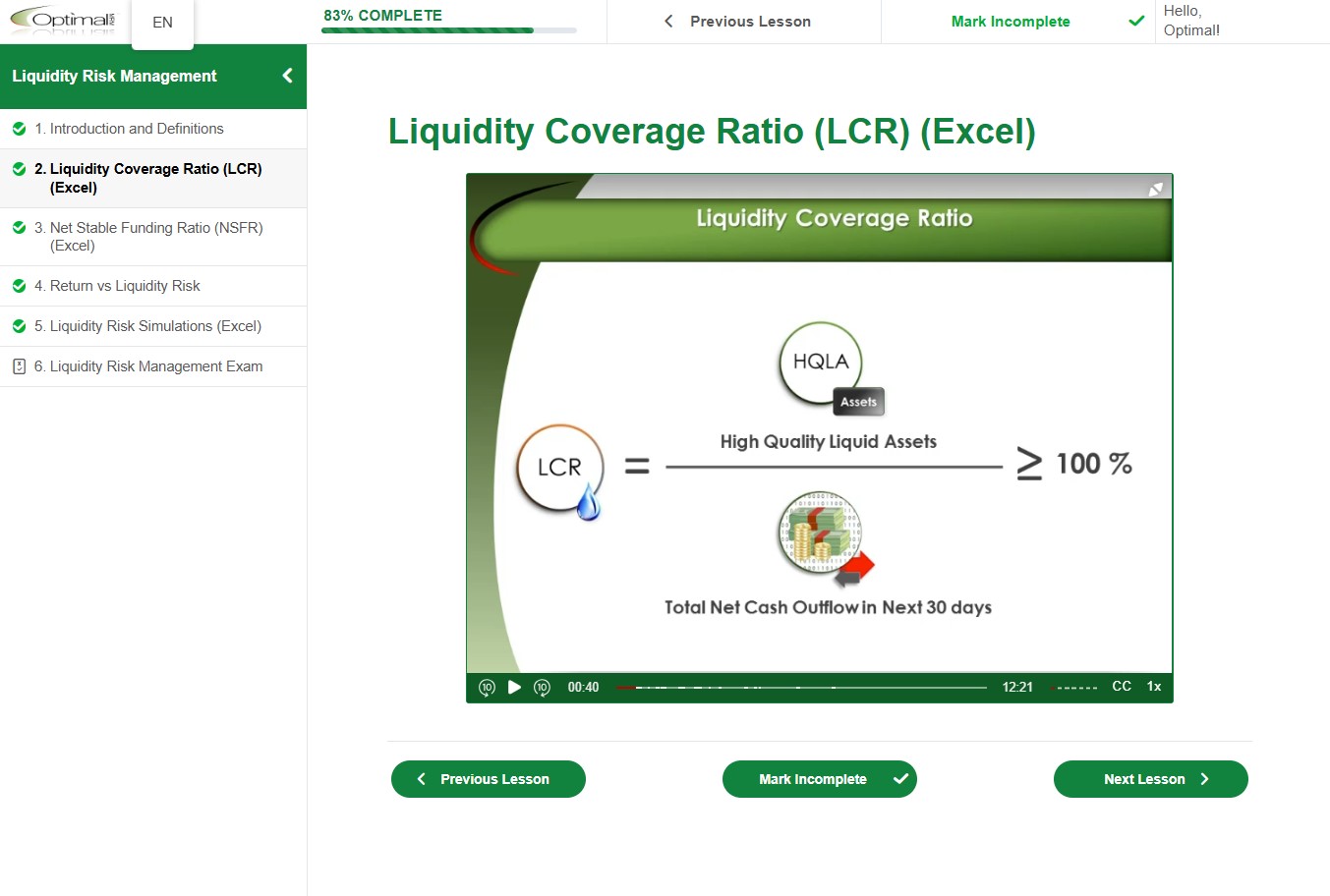

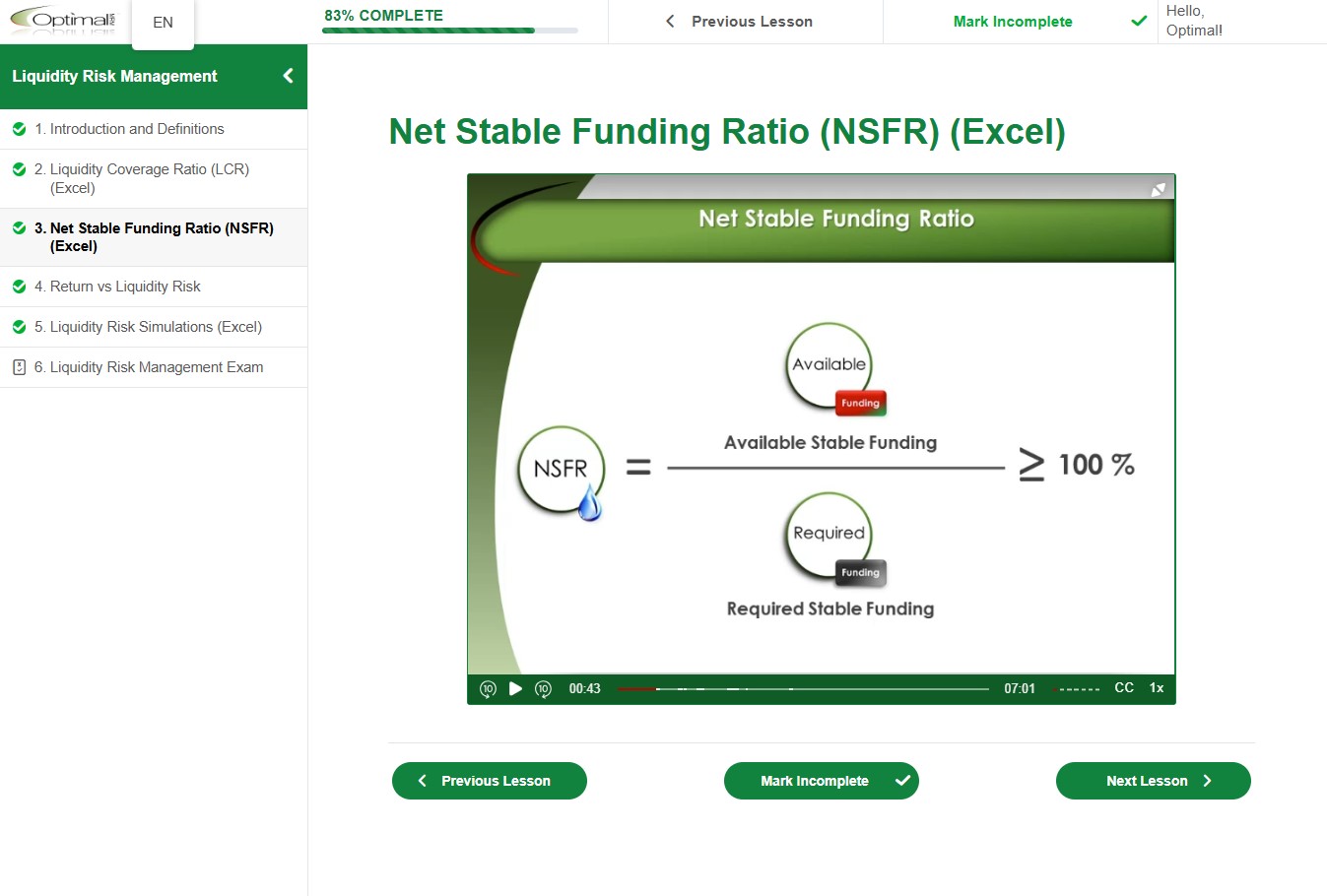

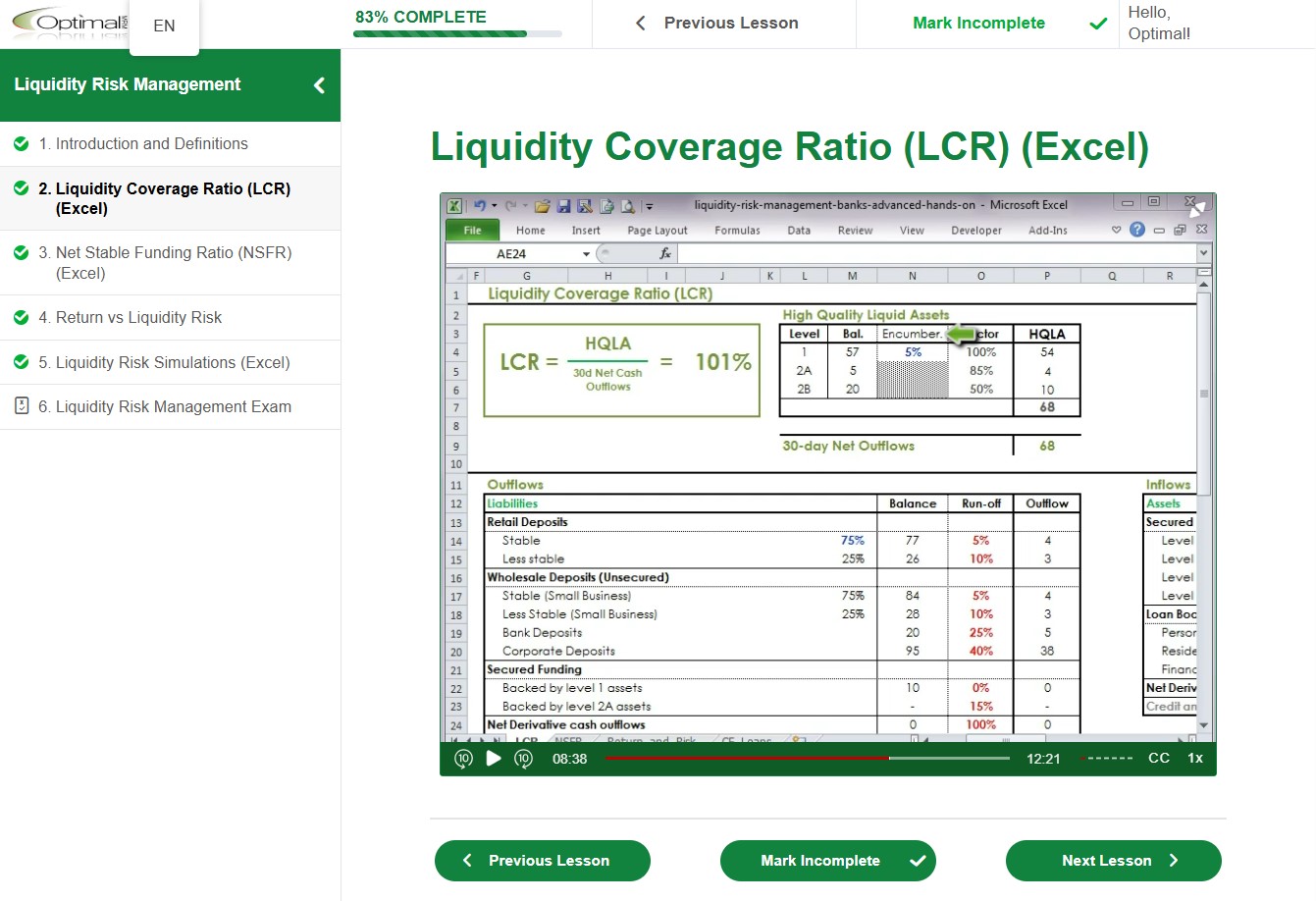

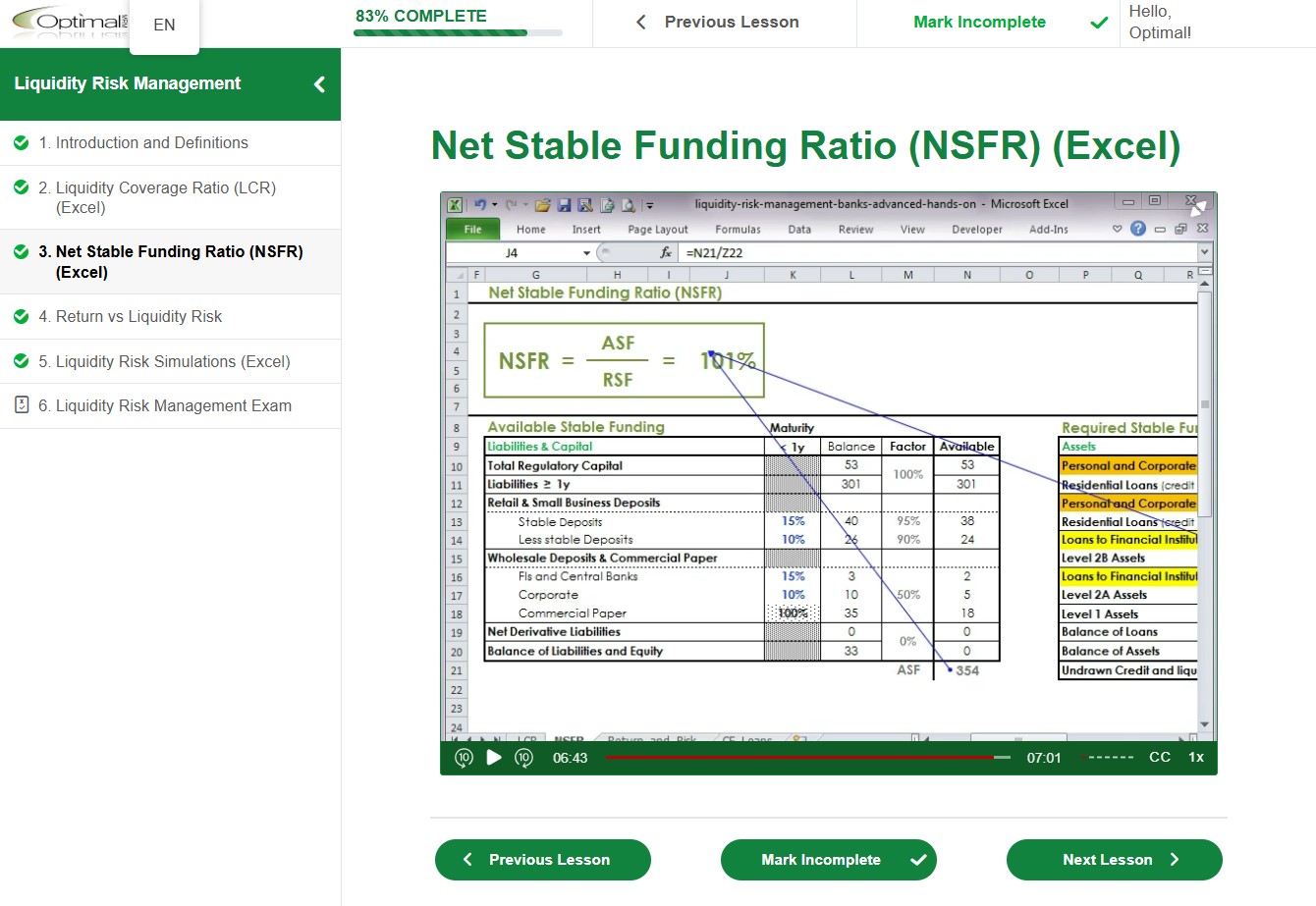

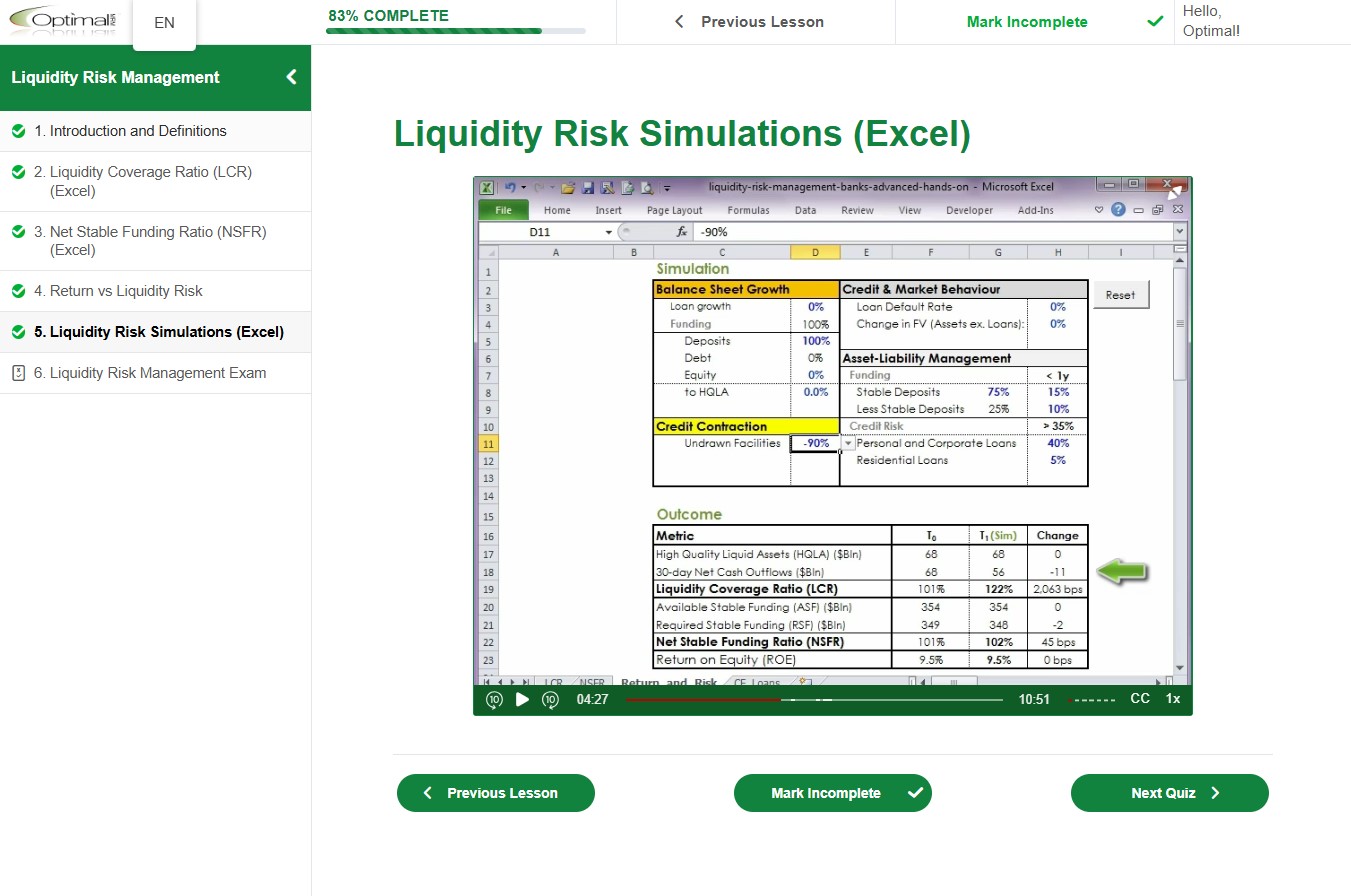

We engage with you in practical exercises in Excel, to measure Basel’s Liquidity and Funding ratios, LCR and NSFR, for a hypothetical bank balance sheet; and simulate the effects of bank strategy, market risk, credit risk, and Asset-Liability Management (ALM) on liquidity and bank performance.

Who Should Enroll:

This course is ideal for risk managers, financial analysts, bank executives, and professionals looking to gain a comprehensive understanding of liquidity risk measurement and management. It is suitable for College and University students who aspire to become risk and finance professionals.

What You Will Gain:

Upon completing this course, you will:

- Acquire a practical understanding of liquidity risk measurement and management principles.

- Differentiate between market and funding liquidity and gain insights into Basel’s regulatory requirements for banks.

- Become proficient in measuring liquidity risk ratios, LCR and NSFR, for a hypothetical bank balance sheet, using Excel as a practical tool.

- Understand the relationship between liquidity risk and bank performance.

- Develop practical skills in simulating the effects of bank strategy, market risk, credit risk, and Asset-Liability Management (ALM) on liquidity and performance, enhancing your risk management abilities.

Duration:

45 minutes

Access Period:

270 days starting from enrollment date.

Ari B. (verified customer) –

Awesome course. You’re just going a bit quick…