Description

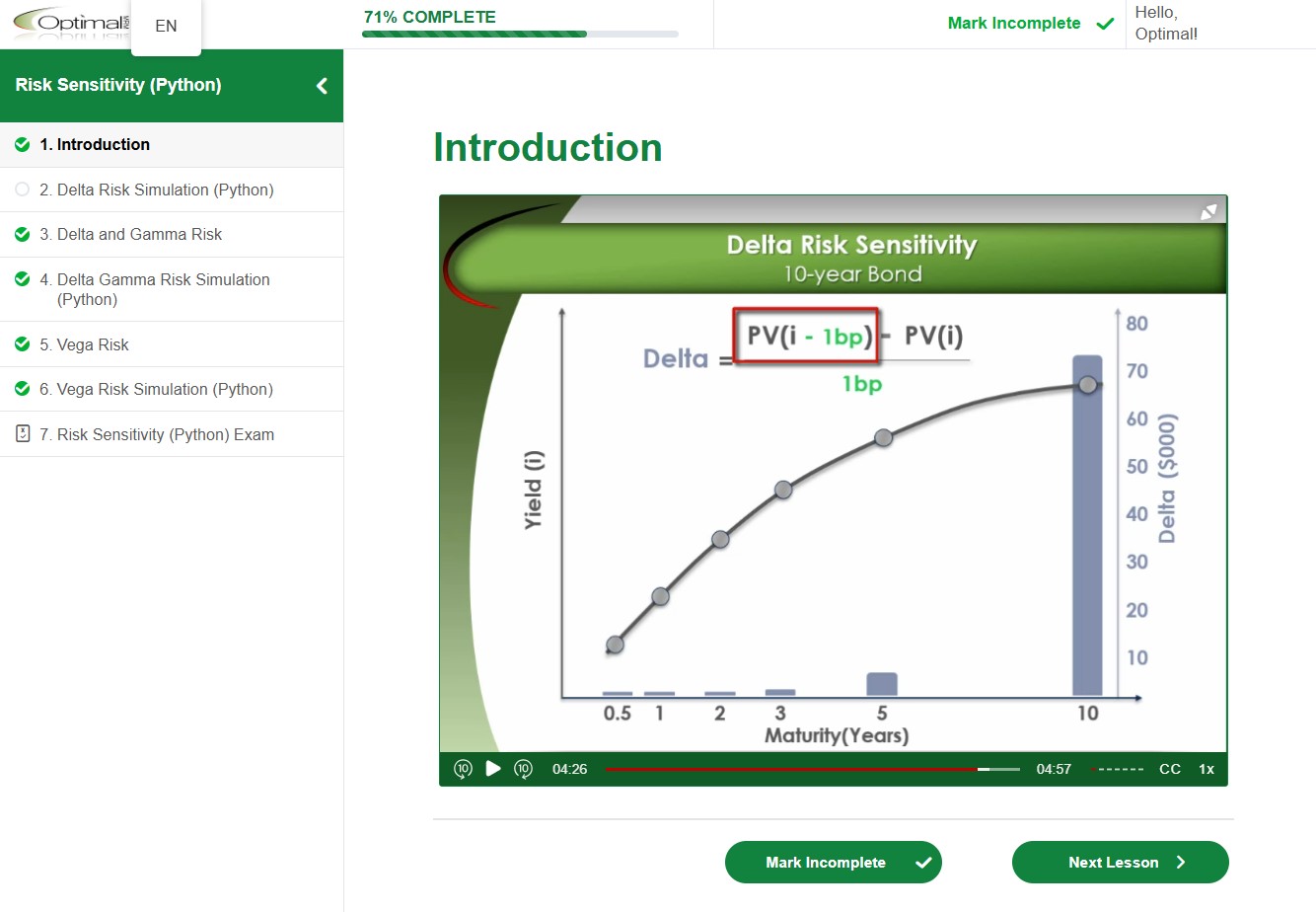

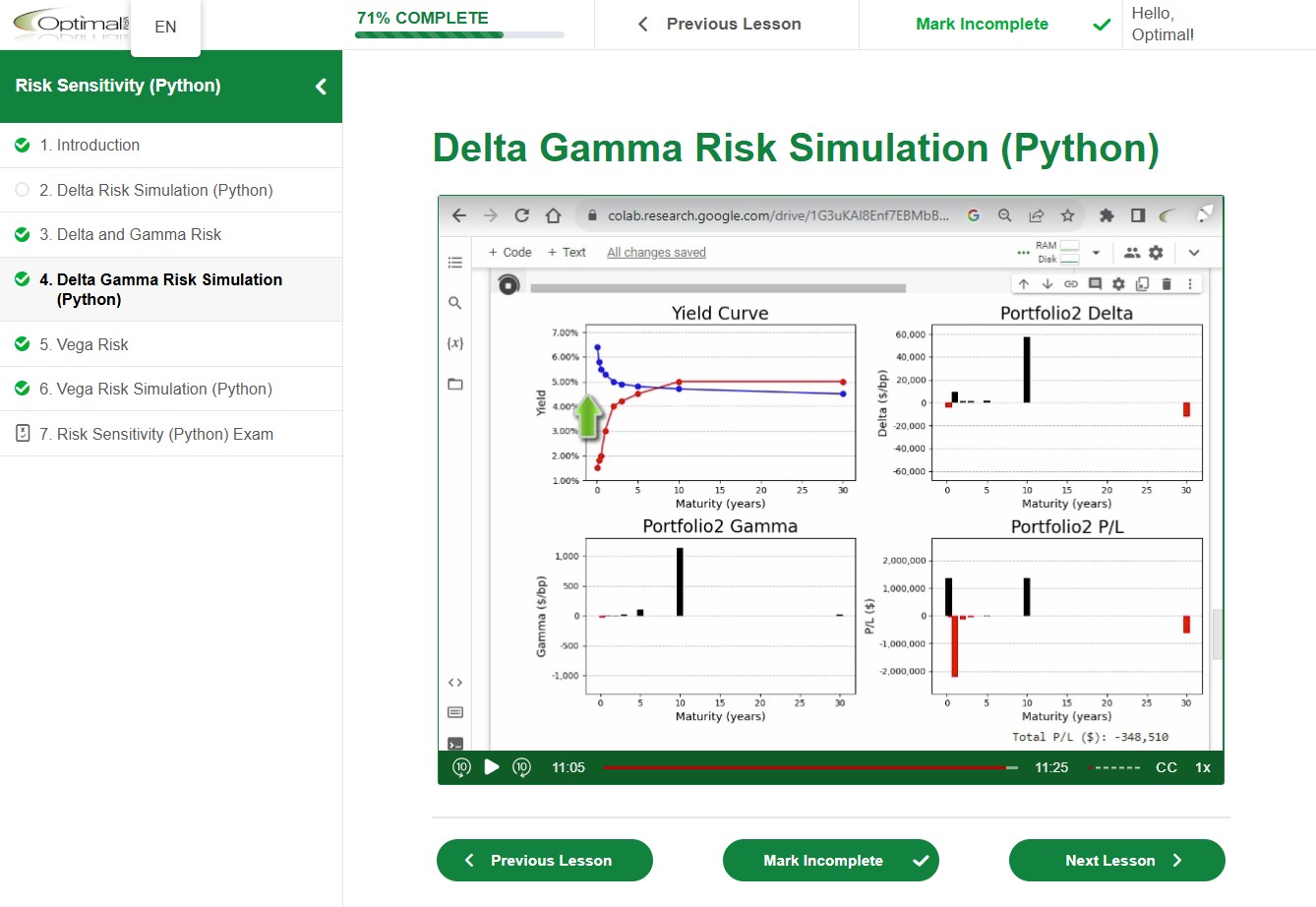

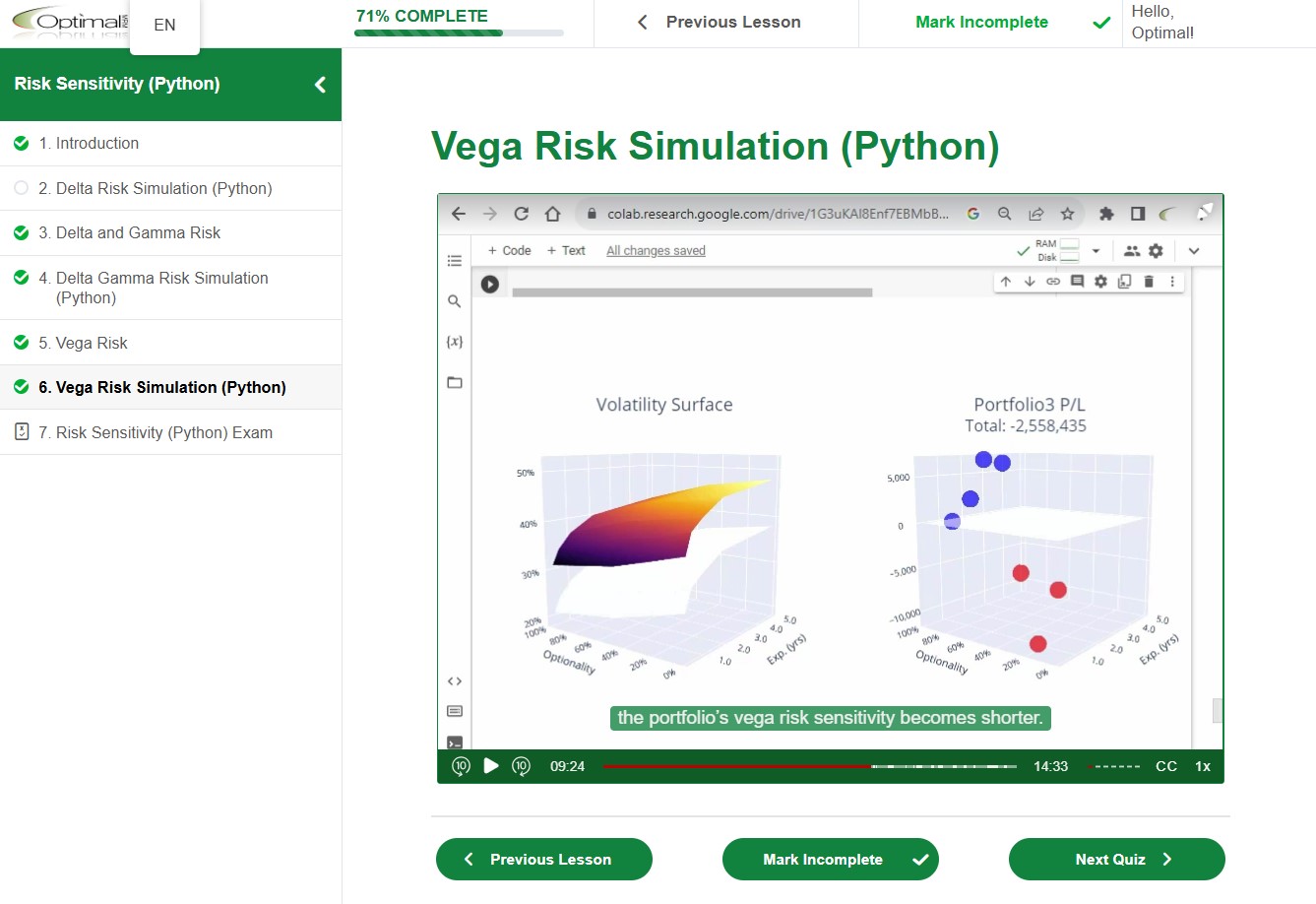

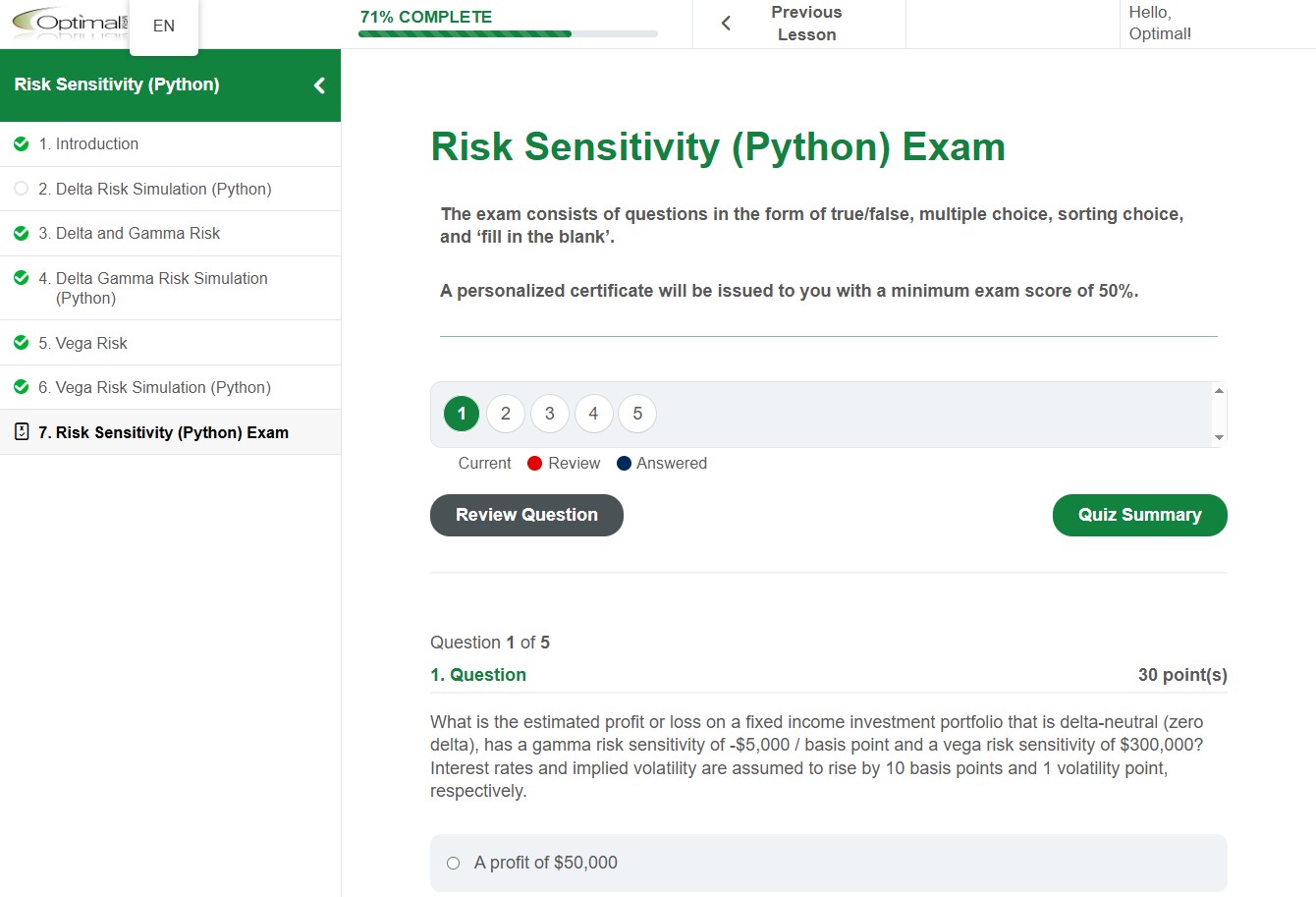

In this e-Learning course, we review the concepts of risk sensitivities, Delta, Gamma, and Vega, presented in the Excel version of the course, and expand on them by using Python to measure risk, and create powerful data visualizations to help us manage risk in rate-sensitive portfolios. We use Python to calculate risk sensitivities for different portfolios of bonds, swaps, and swaptions, and apply them to simulate portfolio profit or loss, as a result of changes in interest rates and option volatility.

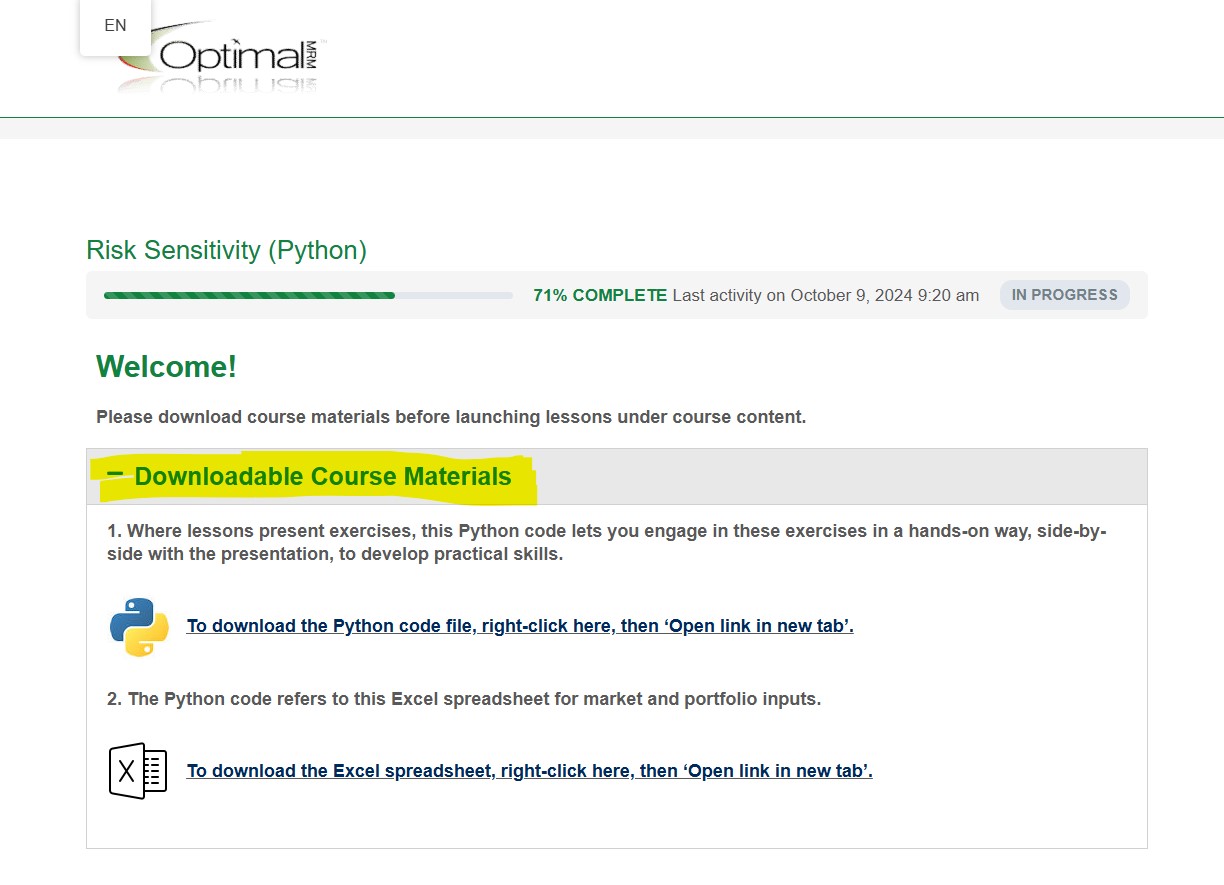

No coding experience needed. Downloadable Python code is included so you can dive right in, as we walk you through course exercises that develop your practical skills, in market risk measurement and management.

Who Should Enroll:

This Python course is versatile and caters to a wide audience. It’s perfect for finance professionals, quantitative analysts, and risk managers looking to bolster their skills in risk management with Python. This course is suitable for College and University students who aspire to become risk and finance professionals with a Python edge.

What You Will Gain:

Upon completing this course, you will:

- Deepen your understanding of risk sensitivities such as Delta, Gamma, and Vega and their application in rate-sensitive portfolios.

- Gain hands-on experience in using Python to calculate risk sensitivities and simulate portfolio profit or loss.

- Learn how to create powerful data visualizations that aid in managing risk in financial portfolios.

- Improve your marketability and employability in the finance and risk management sectors by acquiring practical skills in risk measurement and management using Python.

Duration:

1 hour

Access Period:

270 days starting from enrollment date.

Reviews

There are no reviews yet.